Importance of UX in private banking: interview with Artkai technical advisor Janosh Oros

FinTech ecosystem is rapidly developing to keep the path with recent technological trends, digitalization, and customer needs in the modern environment. We have conducted an interview with Janosh Oros - Artkai technical advisor to find out more about the evolution of Private Banking solutions and their capabilities versus traditional banking.

Q: Janosh, to start with, could you tell us a bit about the history behind FinTech?

Speaking about FinTech and its history, we should state that until 2008 the banking industry was pretty innovative and progressive in terms of solution implementation. There were many constantly emerging products, banking systems, and ecosystems in the market. If we take a look at history, the first examples of innovative banking services were wire transfers, ATMs, and Online Banking. However, such progressive development dramatically slowed down in 2008 when the financial crisis happened.

While the banking industry dealt with the consequences of the crisis - all the other industries were moving forward and evolving in understanding customer expectations and improving the customer experience. Therefore, after decades humanity changed its preferences regarding products or service consumption. When the banks turned their heads back to customers - they realized that the approach they used to offer their services is outdated. The gap between evolved customer expectations and outdated offerings of traditional banks became an opportunity for digitally native FinTechs in the Private Banking sector who started selling traditional banking products through modern engaging and easy-to-use applications.

Q: You’ve mentioned the change in approach to efficient interaction. Why is user experience important in private banking?

When you are used to adding popcorn to your movie ticket and paying for it all together via your smartphone making one click - it is really hard to go back to the age when you needed a calculator to sum up all the costs to come up with a number how much personal banking will cost you per month. In other words - especially in the 21st century, people are driven by the “saw it somewhere - want it everywhere” approach. As an example, I’d like to mention the Chime “Round-Up” feature. When the feature is enabled, Chime automatically rounds up purchases made on your Chime debit card to the nearest dollar and then transfers the difference from your spending account into your savings account. Definitely, you will not be able to make a fortune with this feature but it reflects the trends in functionality people are looking for.

In general, we can say that people are looking for complex scenarios, built on top of traditional private banking services like checking or saving accounts as well as wealth management offerings. The magic here is to make these complex scenarios easy to use creating an excellent user experience.

Q: What are the key drivers, pushing the demand for a better user experience?

Speaking about key drivers I’d like to mention the concept of Digital Maturity. There are 5 levels of Digital Maturity:

- Digitally present - when your business has a website and can be found on the internet.

- Digitally active - when there is a capability to interact with your business through digital channels (here we are speaking mostly about transactional interactions)

- Digitally engaged - this level requires a dramatic shift from the transactional model to the Client Lifetime Value focused one. This means you have to have the following 3 components to succeed: people with the right attitude (company culture), customer-centric business processes, and ready for hypothesis validation and iterative improving digital infrastructure.

- Digitally competitive - if you succeeded on the previous level - your business has a unique asset, not available to competitors.

- Digitally mature - on this level your digital infrastructure evolved enough to give you the opportunity to monetize it using the SaaS model as an example.

As you may see - starting with level 3 the company revenue highly depends on Client Lifetime Value. My experience and industry reports show the fact that a Client's Lifetime depends on the Customer Experience you have. That's why for businesses evolving to the 3rd level of maturity and beyond it is crucial to focus on the quality of their user experience to attract and retain their clients.

Q: Speaking about younger generations, how would you characterize their needs and requirements in terms of coherent UX experience?

To sum up - we can say that younger generations have different product and services consumption cultures. This fact combined with orientation on Client Lifetime Value makes User Experience a key aspect, capable of making a huge impact on business profitability.

Q: Any examples of how others are dealing with this?

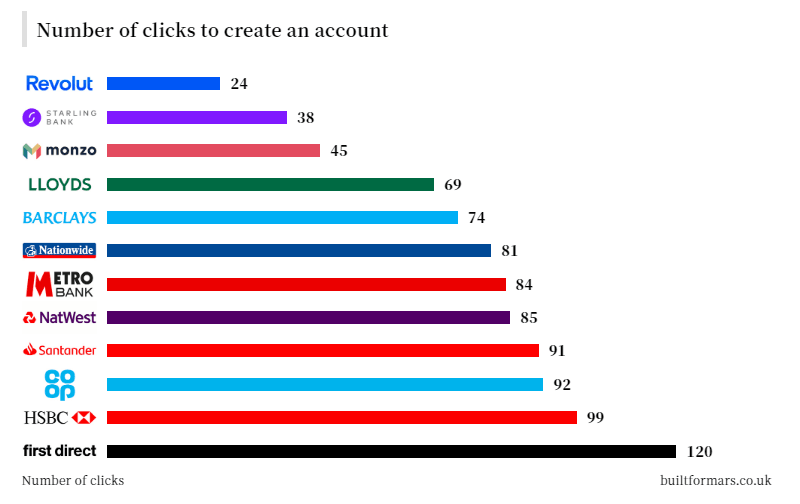

Yes, let’s take a look at the onboarding process in Revolut or TransferWise. There is no need for direct communication with the company members for account opening or registration. Both products have a simple 24/7 available registration process to not lose the opportunity when a client decides to open an account before going to sleep.

It takes only 24 clicks to open a Revolut account and start using it whereas the First Direct traditional bank requires 120 clicks, which is actually 5 times more.

The next evolution is eKYC. As an example - Bahrain has a country-wide blockchain-based Digital Identity which gives a chance to shorten the period of KYC from days to hours and even minutes.

Security though is still at the foremost attention, hence, there won’t be a possibility of any fraudulent activities but a user would be able to start using any services from the very beginning. The speed of deal settlement is one of the approaches to modern usability and friendly customer journeys. Today, a customer doesn’t have to go to the bank, wait in line, and fill out a huge amount of papers. The account opening is now positioned as a commodity rather than a privilege - it should be fast, efficient, and accessible to everyone.

Another great advantage of these FinTech applications is that they grant long-term engagement and beneficial consumption conditions. For instance, Revolut members can receive various discounts and member cards for a range of activities without having to purchase them separately for much higher prices. TransferWise provides 24/7 customer support, low transparent fees, and real-time exchange rates. This ensures cost-efficiency for users and long-term engagement for the company.

Q: How would you categorize the next-generation solutions for Private Banking and what are their differences and benefits?

One of the challenges of the modern FinTech landscape - is fragmentation. Partially the reason is in exit strategy - when startups were created aiming to be acquired by bigger market players. For them the number of clients and revenue needed for company evaluation, not for real long-term value delivery for end clients. Let's put them aside from our today’s conversation and focus on companies that have all the capabilities to cover the full usage scenarios.

These companies can be split into two categories based on solution models:

- Digital Banks/Neobanks that use traditional banks as Back-End

- Independent Platforms that use Open Banking API

If we take a look at the most popular neobanks such as Revolut, Monzo, N26, and Starling - we may see that some of them already experiencing difficulties with growing their number of active clients. The first ones started in a niche with almost zero competition however now there are a lot of players having global expansion as their growth strategy. For them - the similarity of the offering and functionality makes it really complicated to grab another percentage of the clients.

Another factor - they are usually tight to a single bank, acting as a “back-end” for their modern client-facing part. A consequence of such cooperation - is the ability to provide only the “back-end” bank’s products and services.

There are other model-independent solutions utilizing the power of Open Banking. Unlike the first ones they are independent and can offer products and services for various financial institutions. Usually, they provide the ability to connect all your accounts to a single dashboard improving so important User Experience. Such an approach enables the development of even more sophisticated and complex scenarios making the solution more attractive for users.

Q: To sum up, which model is more efficient?

I think both types will survive finding their own audience. However, the independent, platform-like solutions have better capabilities to innovate and offer next-gen services to their clients. No one is interested in having 5 different financial apps on his/her smartphone, switching between them to complete a complex scenario. One multi-functional solution combining all possibilities is the exact way to meet the users’ needs and requirements.

Conclusion

FinTech is constantly developing and growing in its capabilities the results of which we can already see nowadays in Private Banking. People value simplicity and functionality. Enhanced usability, comprehensive user journeys, and multiple scenarios of features integrated into one solution will be the best-match application in terms of user experience. Our team in Artkai manages such application development and helps with UX/UI interface architecture allowing complex and multi-functional interaction establishment. Contact us with any questions!

Clients and Results

Schedule your free consultation

Don't miss this opportunity to explore the best path for your product. We are ready to delve into the specifics of your project, providing you with expert insights and optimal solutions.

Book your free sessionRead More

Explore articles from Artkai - we have lots of stories to tell

Join us to do the best work of your life

Together we advance the human experience through design.